Selling AI to 1.4 Billion People

On June 18, 2026, China Central Television’s official account quietly carried a notice that deserves more attention than it received: eight central government departments, led by MOFCOM, had jointly issued the Implementation Opinions on Accelerating the Development of “AI Plus Consumption” (关于加快”人工智能+消费”发展的实施意见).

The choice of lead agencies is revealing. The document is jointly issued by eight government bodies and led by the Ministry of Commerce rather than regulators more commonly associated with AI governance. Its policy tools are drawn largely from China’s consumption and industrial policy toolkit, including subsidies, financing support, investment funds, and infrastructure development.

In this sense, the document can be understood as the demand-side companion to the State Council’s August 2025 “AI Plus” initiative. The earlier plan focused on expanding AI capabilities across the economy. The new policy focuses on creating markets for AI products and services.

Its intended audience therefore extends well beyond model developers and technology firms. The document addresses manufacturers, retailers, financial institutions, service providers, local governments, and households. Its central concern is how to accelerate the deployment and use of AI technologies across a wide range of commercial and consumer scenarios.

This objective is reflected in the document’s call to “give full play to the advantages of the country’s mega-scale market, broad consumption scenarios, and abundant consumption-data resources.” The formulation is notable because it links AI development not only to technological capabilities, but also to characteristics of the domestic market.

Much of the discussion surrounding AI competition has focused on advanced semiconductors, computing capacity, frontier models, and export controls. These debates are largely organized around the supply side of technological development. The Implementation Opinions place greater emphasis on the demand side.

The underlying logic is straightforward. Large-scale deployment generates revenue, user feedback, operational experience, and application data. These resources can influence product design, model development, and commercial viability. The document explicitly links consumption to the iterative upgrading of AI technologies and products, suggesting that policymakers view adoption not merely as an outcome of innovation, but also as a contributor to it.

For a country with a large domestic market, this can create cumulative advantages. AI phones, AI glasses, intelligent vehicles, service robots, and other consumer products generate continuous streams of real-world interactions. Unlike benchmark evaluations or laboratory testing, these interactions provide information about how users actually engage with AI systems, which functions they value, and which applications prove commercially sustainable.

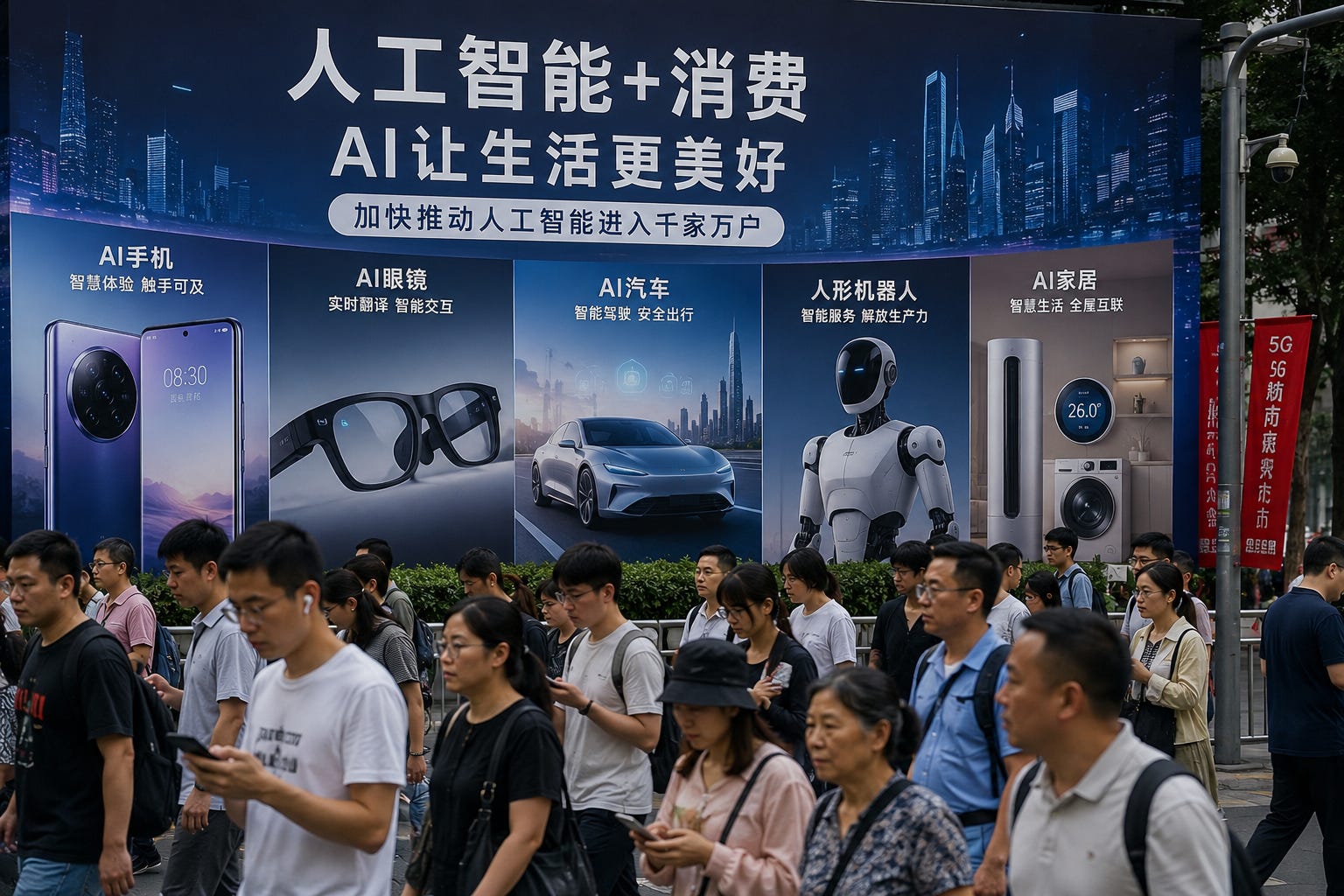

The policy therefore places considerable emphasis on expanding the number of environments in which AI technologies are routinely used. It promotes AI smartphones, PCs, televisions, smart-home devices, wearable products, intelligent connected vehicles, AI glasses, humanoid robots, companion robots, and eldercare robots. It also encourages wider adoption across tourism, hospitality, retail, logistics, education, and home services.

More important than the product categories themselves are the policy instruments supporting them.

The document proposes incorporating AI-enabled products into existing consumer trade-in programs, providing interest subsidies for consumer loans, encouraging dedicated financing products, deploying the National AI Industry Investment Fund, and expanding supporting infrastructure. These measures resemble tools previously used in sectors such as electric vehicles, renewable energy equipment, and consumer electronics.

Taken together, they reduce adoption costs, expand financing availability, and direct capital toward AI-related products and services. Rather than assuming that consumer demand will emerge organically, the policy seeks to shape the conditions under which adoption occurs.

The emphasis on domestic hardware follows a similar logic. Market scale supports production scale. Production scale supports investment, product iteration, and supply-chain development. In sectors where access to advanced foreign technology remains uncertain, domestic demand can help sustain investment and reduce reliance on external markets.

The document does not explicitly frame this objective in geopolitical terms. Nevertheless, a large domestic market for AI phones, AI PCs, intelligent vehicles, wearables, and robotics products inevitably strengthens the broader ecosystem in which Chinese technology firms operate.

A similar pattern appears in the standards section. The document calls for standards covering AI-native devices, interoperability, safety requirements, and intelligence ratings, while encouraging closer alignment between domestic and international certification systems.

This sequence has appeared before in other sectors. Market expansion creates scale. Scale facilitates standards development. Standards can then influence broader industry practices. China’s experience in telecommunications equipment, renewable energy technologies, and electric vehicles demonstrates how market size and standards-setting can reinforce one another over time.

The treatment of governance issues is also noteworthy. Security, safety, and risk management remain present, but they occupy a relatively limited portion of the text. This reflects the function of the document rather than a broader shift in regulatory priorities. Previous AI policies focused on establishing governance frameworks and risk controls. This document is primarily concerned with deployment and commercialization.

Whether the policy achieves its objectives will depend largely on implementation. The scale of subsidies, the design of financing programs, the deployment of state investment funds, local government participation, and consumer willingness to adopt new products will all shape its eventual impact.

More broadly, the document illustrates an increasingly important feature of China’s AI strategy. Alongside efforts to improve frontier capabilities, policymakers are devoting greater attention to diffusion — expanding the use of AI technologies across the economy and embedding them in everyday commercial activity.

The assumption appears to be that technological competitiveness is influenced not only by advances at the frontier, but also by the scale and speed with which new technologies are adopted. In that respect, the domestic market itself is being treated as part of the country’s AI development strategy.

The original CCTV report is available via the AI Plus Consumption notice on the broadcaster’s WeChat account (mp.weixin.qq.com), and the full text of the Implementation Opinions is published on the MOFCOM Market System Development Department site (scjss.mofcom.gov.cn). For the supply-side blueprint this policy operationalizes, see the State Council’s Opinions on Deepening the Implementation of the “AI Plus” Action (August 2025).